Poland

Poland has emerged as a dynamic market over the past 25 years and has become a major player within Europe, being the sixth-largest economy in the EU. In 2017, Poland’s economy expanded 4.6% (OECD), its fastest pace since 2011 and above IMF estimates. Growth was led by domestic demand and government social spending.

This information has been published by Adam Dziedziński

Fleet Meetings

Chapter 1: Economic and business environment

| Demographics | 38,4 million (2017) |

|---|---|

| Capital | Warsaw |

| Major cities | Kraków, Łódź, Wrocław, Poznań, Gdańsk and Szczecin |

| Languages | Polish |

| GDP |

|

| Unemployment rate | 4,8% (February 2018) |

| Main industries | Machinery, Iron and Steel, Coal Mining, Chemicals, Ship Building, Food processing, Glass |

| Currency | Zloty (PLN) |

| Interest rate | 1.5% (March 2018) |

| Fleet Maturity Index (scaling) | |

| Political key info | Poland is a republic based on parliamentary democracy. The country joined the European Union in May 2004. The President (currently Mr. Andrzej Duda) is the head of State, elected by universal suffrage for a five year term. The Prime Minister (currently Mr. Mateusz Morawiecki) is the head of the government. |

| Inflation | 1.6% (April 2018) |

Chapter 2 : Automotive market, segments & sales

| Total Car park |

|

|---|---|

| New vehicle registrations (Cars, LCV, Trucks) |

|

| Top 5 brands (total market) |

|

| Model preference top 5 (total market) |

|

| Used car market/renewal cycle | In 2017 the average age of the vehicle in Poland stood at 13.6 years, while the median age totalled 14 years. The size of the fleet which has been ageing for many years is mainly increased as a result of imports, dominated by cars older than 10 years. |

Chapter 3: Company car market

| Total Fleet Park (company cars)/Fleet penetration in total fleet sales |

|

|---|---|

| Evolution fleet sales (last 5 years) |

|

| Top 5 fleet brands (fleet market) |

|

| Fleet Model preference top 5 (fleet market) |

|

Chapter 4: Taxation & legislation

Get the complete analysis about taxation and legislation in the Fleet Europe Taxation Guide, developed in collaboration with PWC. Click here for more info

4.1 Car taxation

- According to the Polish law, the following taxes/fees are due with regard to cars:

- Value-added tax (VAT);

- Excise duty on passenger cars supplied before their first registration in Poland;

- Car registration fees;

- Tax on transportation means;

- Fee for using the national roads;

- Car registration fees

- Chargeable event: The fee for issuing the registration card along with stickers as well as the fee for issuing number plates are charged every time the vehicle is registered or re-registered (e.g., as a consequence of change of the vehicle’s ownership). Additionally, if the car is registered for the first time in Poland, the fee for issuing the vehicle card is charged.

- Chargeable person: the fees should be settled by a person who is requesting the registration of a vehicle.

- Fee for using the national roadsµ

- Taxable event: The fee for using the national roads is due for vehicles with a certain gross mass (maximum total weight exceeding 3.5t) and buses.

- Taxable person: The fee is payable by a person performing transport on the national roads.

- Tax due: In July 2011 Poland launched the electronic system of charging the fees for using the national roads for transport indicated under relevant provisions. It covers fees due on vehicles with a maximum total weight exceeding 3.5t and buses. The fees are charged based on the distance driven on the road covered by the system and the rates are in PLN per kilometre. The rates vary depending in particular on the

- category of vehicle;

- maximum total weight of a vehicle;

- exhaust fumes emission class.

Persons performing transport on the national roads should possess an electronic device that records the distance covered by a given vehicle.

4.2. Income tax – Taxable persons

- A passenger car is a road vehicle with a maximum total weight of 3.5 tonnes, designed to transport no more than nine persons including the driver except for:

- vehicles having one row of seats separated from the cargo hold with a wall or another fixed partition, classified as multi-purpose cars or vans;

- vehicles having one row of seats with an open cargo hold;

- vehicles having driver’s cabin with one row of seats and cargo hold body as two separate constructions;

- vehicles of a special purpose, e.g., truck-mounted cranes, excavators etc.

- The part of depreciation write-offs calculated on the initial value of a passenger car exceeding the PLN equivalent of 20,000 EUR does not constitute tax deductible cost. Moreover, CIT Law limits the deductibility of insurance premiums for a passenger cars, the value of which exceeds 20,000 EUR (only part of share premiums is tax deductible).

- Based on the Polish CIT Law, the expenditures related to the use of a car, which does not belong to the taxpayer, constitute the tax deductible costs up to the limit calculated as a number of business kilometre travelled multiplied by a rate per kilometre or, in particular cases, up to the monthly lump-sum limit. The above-mentioned expenditures include e.g., fuel or costs of repairs. According to the latest tax authorities’ position the costs of rental payments should be treated as tax deductible without any limitation.

- Regardless of the above, in the case of an operational lease the whole amount of lease fee paid by the lessee constitutes his tax deductible cost.

- Regulations concerning trucks: In the light of the Polish CIT provisions,

- depreciation write-offs and insurance premiums relating to trucks constitute tax deductible costs in full amount and

- costs of use of a rented truck are fully deductible for tax purposes.

- In case of any damage to or liquidation of a vehicle, which was not covered with the voluntary insurance, any losses or repair costs after the car accident do not constitute tax deductible costs.

- Leasing: Below is a summary of general information concerning:

- conditions that need to be fulfilled in order to classify an agreement related to a lease of a vehicle as an operational or financial lease under the CIT Law;

- tax consequences resulting from the above-mentioned classification.

Classification of leasing agreements for CIT purposes

|

| Operational lease | Financial lease |

|---|---|---|

| Period for which agreement must be concluded | A fixed period of time, however, not shorter than two years. | A fixed period of time. |

| Payments | Total amount of lease payments must be equal or higher than the initial net value of the leased vehicle (i.e., net of VAT) or (if the next leasing agreement pertaining to this vehicle is signed) equal to its market value at the date of the next leasing agreement. | Total amount of lease payments must be equal or higher than the initial net value of the leased vehicle (i.e., net of VAT) or (if the next leasing agreement pertaining to this vehicle is signed) equal to its market value at the date of the next leasing agreement. |

| Additional requirements | The lessor does not benefit from the given exemptions listed in the Polish CIT Act. | The leasing agreement needs to include a provision authorising the lessee to depreciate the leased asset for CIT purposes. Consequently, the lessor is not entitled to depreciate the leased asset. |

| Tax consequences resulting from the agreement | The total amount of rental payments constitutes a tax deductible cost for the lessee and taxable revenue for the lessor. Furthermore, the lessor is entitled to depreciate the leased object for CIT purposes. | The capital element of lease payment is effectively tax neutral for CIT purposes for the lessee and lessor. Only the interest element (surplus over the initial value of a leased asset) constitutes tax-deductible cost for the lessee and taxable revenue for the lessor. |

4.3. Company cars

- VAT due on private use of company cars: As a rule, private use of a company’s car by the employee is treated as a taxable supply of services by the employer. In cases where the employee pays no fee for using the company’s car for his/her private purposes, such a use should be considered as a free-of-charge supply of services by the employer, provided that the employer had the right to recover the entire input VAT incurred on the acquisition of goods and services connected with these services. Referring to section 4.2, if the taxpayer has the right to recover only a portion of input VAT incurred on the acquisition of a car, free-of-charge use by employees should not be subject to VAT. If the employee uses the company’s car for his/her private purposes in return for a fee paid to the employer, the employer is deemed to render a rental service to its employee. Additionally, the Polish VAT Law stipulates different methods for determining the taxable amount in case of the private use of the company’s car, depending on whether the employee pays any fee to the employer:

- in the case of free-of-charge use of a company’s car, the taxable amount should be based on the costs of provision of this service borne by the taxpayer (employer)

- in the case of use of a company’s car by the employee in return for a fee, the taxable amount should be equal to the amount due to the employer. Generally, if such a fee significantly differs from the market price, the tax authorities are allowed to establish it for tax purposes on the market level.

In practice, the fee for the use of a company’s car by the employee may be calculated as the number of kilometres driven for private purposes multiplied by a fixed rate depending on the engine size of the vehicle.

- Company cars – income taxes: If for private purposes, the value of this service is treated as a benefit in-kind, which the employee does not pay any fee to the employer for use of a company’s car constitutes his/her taxable income.

Starting from January 1, 2015, the value of received benefit in-kind is fixed and amounts to:- 250 PLN monthly for the use of a car with engine capacity lower or equal to 1600cc;

- 400 PLN monthly for the use of a car with engine capacity above 1600cc.

However, if the employee reimburses his employer for the private use of a company’s car and provided that the said reimbursement is determined in accordance with the arm’s length principle, no benefit in-kind is granted to the employee.

4.4. Income taxes – drivers’ personal taxation

- The vehicle costs made in respect of the private use of a vehicle are not deductible in the employee’s personal tax return.

- The car costs incurred with respect to commuting are not deductible for the employee’s personal income tax purposes.

- In the case when an employee uses his own car for a business trip and the employer refunds the costs of this usage, such a refund does not constitute a taxable income of the employee provided that it does not exceed the limit set for the number of business kilometres driven by an employee multiplied by maximum statutory rate per kilometre, as presented below:

- Cars with engines up to 900cc: 0.5214 PLN/km

- Cars with engines over 900cc: 0.8358 PLN/km

At the same time, the employer may treat the above-mentioned refund as a tax deductible cost up to the limit described above. - In the case when an employee uses his own car for local travel for business purposes and the employer refunds the costs of this usage, in principle, such a refund does not constitute a taxable income for the employee provided that it does not exceed the limit indicated above.

4.5. Electric vehicles

An important barrier to electric vehicle (EV) sales in Poland is the lack of fiscal and tax incentives offered by the Polish government. In the upcoming years this situations will change with the new Act on Electromobility and Alternative Fuels which entered into force on February 22, 2018. Tangible benefits for business owners, included in this act, still wait for the approval of the European Commission.

4.6. Future developments

In 2017 the number of new registered vehicles was the highest since the beginning of the present century and amounted to over 540,000 cars. This was possible due to Poland's good economic situation and significant economic growth. At the same time, however, it is not possible to overlook the positive impact of stable tax regulations on the sale of cars, in particular, in the scope of deduction of VAT related to the purchase and usage of company cars. Keeping the VAT deduction rules introduced in 2014 unchanged (allowing deduction of 50% tax for vehicles used for mixed purposes and 100% tax for sole business purposes) is an important incentive for entrepreneurs.

In 2018, no changes in this matter will take place due to the fact that the current derogation decision issued by the Council of the European Union allows Poland to continue its current restrictions on tax deduction until the end of 2019. Regardless of the issue of VAT deduction from company cars, at the beginning of 2018 a number of other tax regulations essential for entrepreneurs entered into force. Subsequent changes will also be introduced during the current year.

4.7. Legal background (import taxes)

The beginning of 2018 brought many significant changes in the area of corporate income tax (CIT) and personal income tax (PIT). They do not relate specifically to the automotive or fleet industry, however, due to their widespread application to all entrepreneurs, they must undoubtedly also be taken into account by this sector of the economy.

- CIT legislation (the CIT Law in particular):

The Ministry of Finance recently prepared several changes in fiscal regulations that apply to taxpayers paying corporate income tax, or CIT. A complete novelty is the separation of two sources of revenue (income) in the CIT area. Until now, all revenues, regardless of their nature, have been accumulated, and the tax was paid on income based on the sum of revenues and the total costs of obtaining them. From the beginning of 2018, the legislator introduced, as a separate source of revenues, revenues earned from capital gains. - VAT legislation (the VAT Law in particular)

The goods and services tax (VAT) was introduced into Polish tax system in 1993. Regulations in the field of VAT have often been amended in order to harmonise Polish solutions relating to turnover taxes with the current European common system of value added tax. At present, the fundamental legal act in the scope of VAT is the Act of 11 March 2004 on the Goods and Services Tax (the VAT Act). - Traffic Law

The limits shown below apply unless otherwise stated. As road signs may prescribe a lower or a higher speed limit . Different limits apply to cars towing trailers, trucks and buses.

- 50 km/h (31 mph) in built-up areas during the day (from 5 till 23)

- 60 km/h (37 mph) in built-up areas during the night (from 23 till 5)

- 90 km/h (56 mph) on single carriageways

- 100 km/h (62 mph) on dual carriageways or single carriageway expressways

- 120 km/h (75 mph) on dual carriageway expressways

- 140 km/h (87 mph) on motorways

Chapter 5: Car policies

-

Car policies vary between companies. The title of the car lies with its owner. If the company car is leased, its title and ownership lies with the leasing company. If the car is owned by the company, its title lies with it. In the case of mileage or other type of allowance for the use of an employee private car, is the only case when the title lies with the employee. In recent years the usage of cars in Polish companies become shorter. This is due to the good condition of the economy and larger development investments. The lack of qualified workers on the market means that a car often becomes an important benefit for the employee.

5.1 Sectors

Sectors that provide most fleet cars in Poland:- Chemical and Pharma

- Food, beverages and tobacco industries.

- Transport and Communications

- Electricity, gas, water and other utilities.

- Maintenance and security services.

- Professional services

5.2 Job functions

The use of company cars is based on two criteria: function and hierarchy. Related to function, sales forces and staff involved in commercial activities and customer care, are the most common users of company cars. Professional services firms, where the service is provided at the client´s premises are also company car users. From the hierarchy criteria, top management of companies are normal users of company cars, especially in international companies and bigger local corporations. In managerial positions more and more cars are chosen as part of the user chooser policy. The choice is not determined by the cost of purchase, only by the monthly instalment. If the employee wants a better car, he can pay the difference in the instalment.

5.3 Reference cars

The type of cars used for different levels varies significantly among industries. However, common examples of cars used for different levels are: - Entry/junior sales level: B, C segment cars (Skoda Fabia, Ford Focus, Kia Ceed)

- Senior sales / management level D segment cars including crossovers (Skoda Superb, Ford Mondeo)

- Executive level D, E, SUV segment cars (Mercedes E Class, BMW5, Volvo V90)

Chapter 7: Fuel

-

At the end of 2017, Diesel remained the dominant engine, accounting for 2/3 (66.3%) of all vehicles. For several quarters, however, the downward trend in the share of cars with diesel engines has been noticeable. Throughout 2017, the share of Diesel decreased by 4.5%. On the other hand, the popularity of cars powered by gasoline engines grew, which share in the total fleet amounted to 32.7% at the end of 2017 and increased by 3.8% in the previous year. Eco-friendly cars, which are driven by hybrid and electric engines, were still relatively small - their share amounted to 1%. Noteworthy, however, is the dynamic growth of the share of cars with environmental engines - in 2017 has more than tripled.

- Fuel type segmentation

Diesels (66.3%)

Petrols (32.7%)

Alternative fuels (1%)

- Fuel infrastructure

Polish network of filling stations at the end of 2017 covered 6,640 outlets. This number of filling stations is smaller than at the end of 2016 by approximately 160 stations.

- Fuel card solutions

Fuel card volumes have grown annually in Poland between 2014 and 2017 due to an inflow of new fleet and CRT cards being issued over this period as they attempt to reduce transport costs. Value of the Polish fuel card market rose by over 16% in 2016 as a result of new cards issued and an increase in both petrol and diesel prices, after prices. Market value will grow annually towards 2022 as fuel prices are forecast to rise by €0.12 over the next five years on an average per litre, which will force many domestic fleets to turn to fuel cards in an attempt to keep transport costs low. The most popular fuel cards in Poland include: PKN Orlen Flota, LOTOS BIZNES, BP PLUS Routex, euroShell , DKV. -

Chapter 9: Safety, insurance and telematics

- Accident rate and evolution

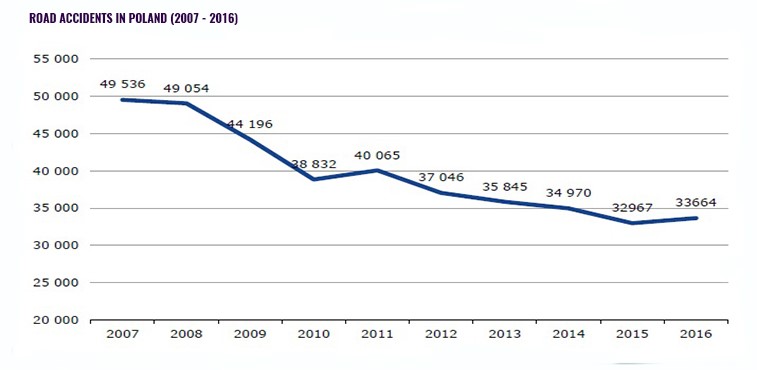

Statistics of road accidents in Poland are not optimistic. Polish roads still belong to one of the most dangerous in the European Union. Despite this fact, 2017 was a really good year in regards to road safety. Number of fatal accidents on Polish roads last year did not exceed three thousands. This is the best result in over 30 years. According to the Polish police in 2017 there were 33 350 car accidents in Poland. As many as 86% of them caused by drivers' fault, who most often violate the right of way (25% of all accidents), exceed allowed speed (24%) and perform dangerous maneuvers that end at least with a collision (16%). Every day in road accidents are also involved many drivers who are on the business trip. Half of managers in Poland admit that their subordinate caused or was involved in an accident by driving a car during a business trip.

-

Insurance offers (calculation) and suppliers

In recent years we have witnessed the increase of insurance premiums on the Polish market. This is due to the higher awareness of clients and the activity of insurance claim law companies. The industry market has also decreased. This is a change that primarily affected the fleet insurance market in Poland. At the end of 2015, “Link4” was bought by ”PZU”.

And while the “Link4” brand on the retail market and sales under this brand was maintained, the insurer disappeared completely from the fleet market. The same happened with company called “Liberty Ubezpieczenia” , which was bought by “AXA”. In this way, less than 2 years after the debut on the fleet market, “Liberty” ceased to insure the fleet clients. “Generali” was another company that resigned from fleet insurance. Three competitors have disappeared from the market. And many other insurers reduced their activity - either by withdrawing from specific industries (international transport, car rental), or by limiting their activity to maintain the current portfolio, without offering new options.

Telematics availability

Polish market used to be dominated by local medium and small businesses. In the last two years we have seen consolidation on the market and the largest Polish companies were taken over by foreign players - Finder became part of TomTom Telematics, and Viasat took over CMA. Telematics market also gained new growth dynamics throughout the introduction of an act imposing the obligation of road transport monitoring . The new act is primarily designed to seal the VAT system, thus marginalizing the financial benefits of the “grey area”. Consequently, the new law imposes additional obligations on operators that transport certain articles. Among fleet managers, telematics is constantly gaining on popularity, as the awareness of the possibilities offered by the use of comprehensive telematics solutions in fleets is also growing.